We don't expect any further shift in tone with the stage set for rate cuts soon…

Publicada el jueves, 25 de enero de 2024 | Actualizada el viernes, 1 de marzo de 2024

We don't expect any further shift in tone with the stage set for rate cuts soon…

Resumen

… but we now anticipate an even more gradual easing cycle due to Banxico's caution xxxxxxxxxxxx xxxxxxxxxxxxxxxxxxxxx xxxxxxxxxxxxx x

Puntos clave

- Puntos clave:

- In our previous note following November's Banxico decision (see), we highlighted a significant shift of tone in the statement that suggested that discussions among Board members on avoiding a more restrictive stance in the coming months had started

- While the Board has warned that rate cuts early next year won't necessarily mark the beginning of an easing cycle, we suspect a further deceleration of core inflation will eventually convince them to signal the beginning of a normalization cycle sooner rather than later. I

- ecessarily be facing a cycle of continuous decreases. Banxico is thus set to hold the policy rate at 11.25% and stick with its message that, with the disinflation process on track, it will likely cut the nominal policy rate in early 2024 to avoid an unwarranted further increase in the real ex-ante rate.

-

In our previous note following November's Banxico decision (see), we highlighted a significant shift of tone in the statement that suggested that discussions among Board members on avoiding a more restrictive stance in the coming months had started. The meeting minutes released a couple of weeks ago confirmed this. One member argued tñlhat, considering the recent improvements in the inflationary outlook, “there is room to discuss cuts to the reference rate,” while another one echoed this opinion by stating that “the possibility of adjusting the reference rate downwards could begin to be evaluated in the policy meetings of the first quarter of 2024.” Although this view was not unanimous, as one member emphasized that Banxico “must not drop its guard” and warned that “it [was] neither prudent nor necessary to bring forward a signal that could change soon” in face of inflationary risks that continue to be biased to the upside, it seems that a large majority is beginning to form within the Board towards starting to gradually cut the nominal policy rate as soon as in February.

-

While the Board has warned that rate cuts early next year won't necessarily mark the beginning of an easing cycle, we suspect a further deceleration of core inflation will eventually convince them to signal the beginning of a normalization cycle sooner rather than later. In recent weeks, Deputy Governor Jonathan Heath has expressed that the expected rate cuts early next year must be read as representing a shift from a “passive” to an “active” monetary-policy tightening approach. While the passive phase has involved holding the nominal policy rate unchanged at its current 11.25% level for several months, the ongoing improvement of inflation expectations will soon compel Banxico to transition to an active phase whereby the policy rate will require "fine-tuning" adjustments to avoid an overly restrictive monetary stance as measured by the real ex-ante policy rate. The Board November’s meeting minutes also shed some light regarding this likely strategy, with one member even suggesting that, in the “next months, [the real ex-ante policy rate] should be maintained between 7 and 7.5%.” Governor Victoria Rodriguez has also given her approval to these potential movements, by recently stating that if rate cuts occur in 1Q24, they “would be gradual” and Banxico “would not necessarily be facing a cycle of continuous decreases.

-

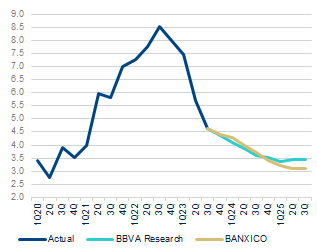

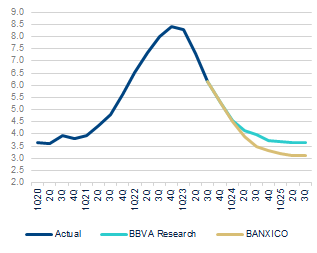

Banxico is thus set to hold the policy rate at 11.25% and stick with its message that, with the disinflation process on track, it will likely cut the nominal policy rate in early 2024 to avoid an unwarranted further increase in the real ex-ante rate. Even if core services inflation has continued to show stickiness (Figure 2), core inflation has continued to come down broadly in line with Banxico’s most recent expectations (Figure 4), and the disinflation pace remains relatively fast—after dropping (-)1.1 pp in 3Q, it is set to further ease (-)0.7pp in 4Q. Since last month’s meeting, both 12-month headline and core inflation expectations came down 0.1 pp to 4.1%. We continue to think they have plenty of room to come down further (our current 12-month expectations are 3.4% and 3.7% for headline and core inflation, respectively). We expect core inflation to fall to levels close to 4.0% by late 2Q24 but to drop below that threshold until 3Q24. Yet, with inflation dropping back, the real ex-ante rate is not only set to remain very high but to most likely continue increasing in the coming months.

-

Thus, we think that Banxico is likely to start to “fine-tune” the monetary policy stance and cut the policy rate by 25 bps to 11.0% in the first meeting of next year (likely in early February) to avoid an unwarranted increase in the policy rate. Although we think that Banxico should not skip rate cuts at any meetings next year, its cautiousness, hawkishness, and recent hints (see paragraph above) suggest that consecutive rate cuts are unlikely at the start of the gradual easing cycle. Thus, although in our baseline scenario a further delay in the start of the easing cycle is no longer necessary, we now anticipate an even more gradual easing cycle due to Banxico's cautiousness. We now expect Banxico to bring down the policy rate to 9.0% by year-end 2024.

Temáticas

- Etiquetas de Temática

- Bancos Centrales

Etiquetas

- Etiquetas

- Indicadores económicos

- Banxico

- Tipo 1

- Macroeconomía